income tax has always been a key issue in corporate restructuring. On April 30, 2009, the Ministry of Finance and the State Administration of Taxation jointly issued the Notice on Several Issues Concerning the Treatment of Enterprise Income Tax on Enterprise Restructuring (Caishui (2009) No. 59), which is the first time in the field of tax law to define enterprise restructuring, and the so-called enterprise restructuring refers to the transaction in which the legal structure or economic structure of an enterprise changes significantly outside its daily business activities, including changes in the legal form of the enterprise, debt restructuring, equity acquisition, asset acquisition, merger, separation and so on. Document No. 59 also clarifies the rules for the tax treatment of corporate and corporate shareholders' income tax. However, in the practice of corporate restructuring, the issue of personal tax obligations of natural person shareholders is often not paid attention to and clarified. Based on the two reorganization methods of enterprise merger and separation, this paper discusses whether the natural person shareholders of the merged and separated enterprises should pay personal income tax.

1. major tax laws and policies

2. Inland Revenue Department official consultation reply collation

3. this article to share ideas

4. thoughts and suggestions

the merger/separation of enterprises mainly involves the income tax treatment of two subjects: one is whether the losses of the merged/separated enterprises can be carried forward in the merged/separated enterprises; The second is how the shareholders of the merged/separated enterprises should pay income tax. Shareholders can be either legal persons or natural persons, but there is an imbalance in the current income tax policy between the two types of shareholders.

1. Corporate Income Tax Area

Caishui (2009) No. 59 has two provisions on the income tax treatment of corporate shareholders: general tax treatment and special tax treatment.

In a business combination/separation, there is usually a change in equity ownership. Generally, tax laws require recognition of gains or losses from equity changes, and shareholders are subject to income tax on the benefits of equity mergers/demerger, which is the logic of general tax treatment. However, there are also some enterprises that have not changed their mode of operation and content before and after the merger/separation, and the transaction process does not involve or rarely involves monetary payment. Therefore, the purpose of such corporate restructuring is not to transfer assets for profit, but to optimize the allocation of resources, strengthen the competitiveness of enterprises in the market, shareholders' rights and interests have not changed substantially. If shareholders are taxed, it will increase transaction costs, be detrimental to the competitive development of a market economy and violate the principle of tax neutrality. Therefore, No. 59 provides that such enterprises may choose special tax treatment: that is, to meet certain applicable conditions of restructuring transactions, the corporate shareholders of the equity payment portion of the current recognition of disposal gains and losses, until the future corporate shareholders will transfer the equity to confirm the taxable income.

On July 26, 2010, the State Administration of Taxation issued the" Administrative Measures for Enterprise Income Tax on Enterprise Restructuring Business "(State Administration of Taxation Announcement No. 4 of 2010) further stipulates that all parties involved in the same restructuring business shall adopt The principle of consistent tax treatment, that is, unified tax treatment according to general or special tax treatment.

2. Personal Income Tax Area

regarding the question of whether natural person shareholders involved in enterprise merger/division can apply general tax treatment or special tax treatment and how to distinguish between general tax treatment and special tax treatment, the tax law and tax policy have no clear provisions for the time being. it is only mentioned in the" announcement on several issues concerning the collection and administration of enterprise income tax for enterprise restructuring business "(announcement of the state administration of taxation no 48 of 2015) issued by the state administration of taxation in June 2015. The announcement clearly states: "In a restructuring transaction, the transferor in the equity acquisition, the shareholders of the merged enterprise in the merger and the shareholders of the divided enterprise in the division may be natural persons. Natural persons among the parties shall be taxed in accordance with the relevant provisions of the personal income tax."

2. & nbsp; Inland Revenue Department Official Consultation Reply Summary

We found a total of 13 answers to related questions through the online message module of the State Administration of Taxation 12366 Tax Service Platform. The views of local tax bureaus can be classified into the following two categories:

1. In a business combination/division, if an individual shareholder is involved in the transfer of equity or investment in non-monetary assets, he or she shall pay personal income tax in accordance with the item" income from the transfer of property "; if it involves the distribution of retained profits, he or she shall pay personal income tax in accordance with the item" income from interest, dividends and dividends.

2, with reference to non-monetary asset valuation appreciation treatment, that is, mainly to see whether the separation of the enterprise's paid-in capital changes, if the paid-in capital increases on behalf of non-monetary assets appreciation, subject to personal income tax. Whether it is a split or a merger, if the original value of the individual's original equity is less than the original value of the new enterprise's equity, there is an increase in value and personal income tax is required.

3. this article to share ideas

judging from the above reply results, the settlement standards of tax authorities in different regions are not consistent. Even in accordance with the requirements of the tax authorities, how to determine whether natural person shareholders involved in equity transfer and other acts, still face the difficulty of unified interpretation. Not only that, there is a view in current practice: No. 48 is a document that regulates corporate income tax, so it cannot be applied to natural person shareholders. For changes in the ownership and equity of shareholders involved in the merger/division of a natural person shareholder, the gain or loss on the disposal of assets shall be recognized at fair value and personal income tax shall be paid. We believe that this view is inevitably biased, and the determination of whether a natural person shareholder is required to pay a tax should be returned to the provisions of the Personal Income Tax Law, I .e., based on the determination of whether the equity held by a natural person shareholder has increased in value or whether an equity transfer has occurred. The following examples are discussed:

Case 1: After the merger/separation of the enterprise, the shareholding ratio of natural person shareholders remains unchanged, and the cost of shareholding investment (tax basis) remains unchanged

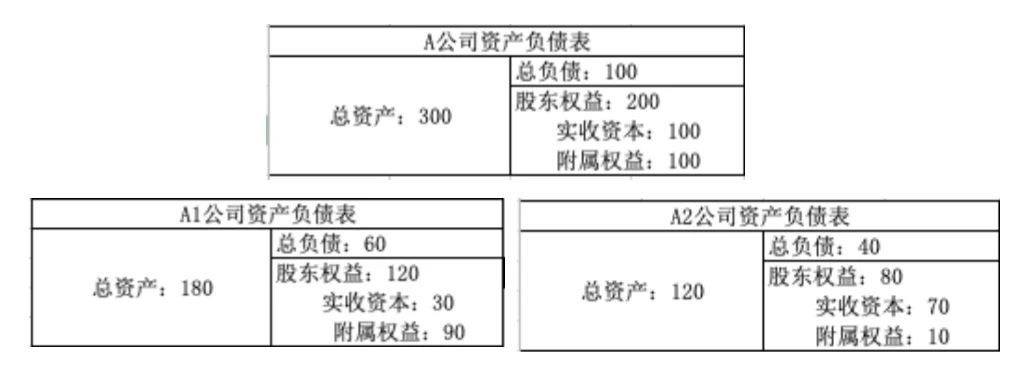

Example 1-1: Company A has paid-in capital of 1 million yuan, and natural person shareholder A has paid-in 600000 yuan to hold 60% of the equity. A company is divided into A1, A2 two companies. The paid-in capital of Company A1 is 300000 yuan, and the paid-in capital of Company A2 is 700000 yuan. A1 and A2 inherit assets and liabilities in proportion and do not exceed the business scope of Company A. A continues to hold 60% equity of Company A1 and A2 respectively.

Analysis: From an economic point of view, Company A is divided into two companies, which is equivalent to dividing the rights and interests controlled by Shareholder A, however, the investment cost (tax basis) of the equity held by A has not changed & mdash;& mdash; After the separation, the shareholder is still A, the shareholding ratio is still 60%, and the shareholding cost (tax basis) is still 600000 yuan. Therefore, we believe that before and after the division/merger of the enterprise, under the condition that the shareholding ratio of shareholders remains unchanged and the investment cost of shareholding remains unchanged, natural person shareholders are not involved in personal tax obligations. However, the amount of non-equity payment obtained by means of monetary funds and exceeding the investment cost (tax basis) of the equity held shall be regarded as profit distribution, and natural persons shall pay personal tax according to the items of "interest, dividend and bonus income.

If the separated enterprise does not divide its assets and liabilities in proportion, are natural person shareholders liable to pay taxes? The analysis is as follows:

same example 1-1, before the division, company a's total assets were 3 million yuan, total liabilities were 1 million yuan, and total shareholders' equity was 2 million yuan: including paid-in capital 1 million yuan, capital reserves, surplus reserves, etc. total 1 million yuan (hereinafter referred to as" subsidiary equity "). Company A has a 3:7 split equity investment cost (tax basis), I .e. the paid-in capital of Company A1 is 300000 yuan and the paid-in capital of Company A2 is 700000 yuan, but A1 and A2 inherit the assets and liabilities of Company A according to a ratio of 6:4, and Company A holds 60% equity of Company A1 and Company A2 after split:

Analysis: Although the subsidiary rights and interests of shareholders are not distributed at the ratio of 3:7 due to the uneven distribution of assets and liabilities, in economic essence, the investment cost (tax basis) of the company's equity held by A after the separation is still 600000 yuan, the corresponding amount of shareholders' equity is still 1.2 million yuan, and the shareholders' equity has not changed. We believe that the analysis in Example 1-1 is still consistent with the conclusion that the natural person shareholder is not involved in a tax liability. However, if we look in depth, the inconsistency between the paid-in capital split ratio and the asset-liability split ratio in the process of enterprise separation actually involves the issue of changes in the risk of repayment of the company's creditors, which will not be discussed in depth here.

Scenario 2: After the merger/separation of the enterprise, the proportion of shares held by natural person shareholders changes, and the cost of holding investment remains unchanged

Analysis: Although the subsidiary rights and interests of shareholders are not distributed at the ratio of 3:7 due to the uneven distribution of assets and liabilities, in economic essence, the investment cost (tax basis) of the company's equity held by A after the separation is still 600000 yuan, the corresponding amount of shareholders' equity is still 1.2 million yuan, and the shareholders' equity has not changed. We believe that the analysis in Example 1-1 is still consistent with the conclusion that the natural person shareholder is not involved in a tax liability. However, if we look in depth, the inconsistency between the paid-in capital split ratio and the asset-liability split ratio in the process of enterprise separation actually involves the issue of changes in the risk of repayment of the company's creditors, which will not be discussed in depth here.

Scenario 2: After the merger/separation of the enterprise, the proportion of shares held by natural person shareholders changes, and the cost of holding investment remains unchanged

Example 2: company a's paid-in capital is 1 million yuan, natural person shareholder a paid-in 600000 yuan holds 60% of the equity, and B holds 40% of the equity paid-in 400000 yuan. Company A is divided into Company A1 and Company A2. Company A1 has paid-in capital of 300000 yuan and Company A2 has paid-in capital of 700000 yuan. Company A1 and A2 have not changed the business essence of Company A. Company A holds 70% equity of Company A1 and Company A2.

Analysis: regarding the 60% equity part originally held by a, the same as example 1; As for the newly acquired 10% equity part of A, since the paid-in capital has not changed, the capital increase and share expansion can be excluded, so in essence, A has transferred 10% equity from B. B the transfer of 10% of the equity, in accordance with the State Administration of Taxation Announcement No. 67 of 2014 to determine whether the need to declare and pay tax; A newly acquired 10% equity, according to its payment consideration method (whether the consideration, what kind of consideration) to judge whether the need to declare and pay tax.

scenario 3: after the merger/separation of the enterprise, the shareholding ratio of natural person shareholders remains unchanged and the total paid-in capital changes

Example 3: company a's paid-in capital is 1 million yuan, natural person shareholder a paid-in 600000 yuan holds 60% of the equity, and B holds 40% of the equity paid-in 400000 yuan. Company A is divided into Company A1 and Company A2. Company A1 has paid-in capital of 1 million yuan and Company A2 has paid-in capital of 1 million yuan. Company A1 and A2 have not changed the business essence of Company A. Company A holds 60% equity of Company A1 and Company A2.

Analysis: it needs to be discussed according to different situations:(1) if the increase in the investment cost of a's shareholding is added in cash, there is no need to pay personal tax at the investment stage;(2) If the increase in paid-in capital is due to the conversion of capital reserve or surplus reserve into capital: 鈶?In the case of conversion of capital premium, we think that A does not need to pay personal tax (although local tax);鈶?to other capital reserves or surplus reserves to increase the paid-in capital, we believe that the economic essence should be broken down into the enterprise's dividends to shareholders and shareholders with dividends to increase the capital of two transactions, A needs to be in accordance with the" interest, dividends, dividend income "item declaration and payment of tax.

Scenario 4: After the merger/separation of the enterprise, the shareholding ratio of natural person shareholders changes and the total paid-in capital changes

Example 4: in the same example 3, after the separation, the paid-in capital of A1 company is 1 million yuan, the paid-in capital of A2 company is 1 million yuan, A1 and A2 have not changed the business essence of company a, and the proportion of shares held by a in company A1 and A2 has changed to 40% respectively.

Analysis: There are two reasons for the decline in A's shareholding:(1) A's transfer of 20% of the equity to B;(2) B's capital increase and share expansion led to a decline in A's shareholding. For equity transfer, the provisions of the State Administration of Taxation Announcement No. 67 of 2014 shall be applied to the judgment, which will not be repeated here. Regarding the personal income tax involved in the capital increase and share expansion of B, we have written articles to discuss the personal income tax. for details, please refer to discussion on whether individual shareholders need to pay personal income tax for capital increase and share expansion-taking the consultation reply of Guangdong Zhanjiang tax bureau as an example .

In particular, the above example is discussed by the separation of enterprises. Regarding the personal tax of natural person shareholders involved in the merger of enterprises, the analysis and judgment is made with reference to the change and invariance of the split shareholding ratio and the cost of ownership (tax basis), which will not be repeated in this article.

4. thoughts and suggestions

Looking at the content of No. 59, the core of the document is to determine which conditions have been reached to determine that the reorganization transaction has the essence of optimizing the allocation of resources, so that the legal person shareholders can apply special tax treatment. So the core of the problem is that the enterprise income tax law does not give law enforcement agencies the power to tax the optimal allocation of resource-based restructuring transactions. Therefore, No. 59 is not to solve the problem of whether corporate shareholders should pay taxes, but to solve how to determine whether it belongs to the optimal allocation of resource-based restructuring transactions.

Similarly, even if there is no similar standard in the personal income tax law, it does not mean that natural person shareholders must pay a tax. Combined with the above case analysis results, we believe that the judgment standard of personal income tax in practice should not be lower than that of enterprise income tax, otherwise it will appear in the same enterprise. Legal person shareholders do not need to pay enterprise tax, but natural person shareholders need to pay individual income tax. There are completely different income tax treatments for the same economic business, which actually violates the principle of tax fairness.

In summary, we suggest that the tax authorities should comprehensively and carefully consider the consistency of the tax obligations of corporate shareholders and natural person shareholders at the income tax level, and issue relevant regulations at an early date to regulate the scale of enforcement in such cases. At the same time, we recommend that enterprises do a good job in the overall planning and design of the transaction model and tax-related parts of the transaction documents before the merger/separation, in order to safeguard the rights of taxpayers and reduce subsequent tax risks in accordance with the law.

creation and approval: Wang Yongjing

senior partner of shengdian law firm, director of shengdian tax law research center, registered lawyer of hong kong kewushen law firm (ONC) (Chinese law), arbitrator of south China international economic and trade arbitration commission (Shenzhen international arbitration court), expert of third-party supervision and evaluation mechanism of compliance of enterprises involved in Guangdong province, instructor of master's degree in legal cooperation of central south university of economics and law, off-campus tutor of Master of Law from Law School of Shenzhen University, member of Tax Law Professional Committee of All China Lawyers Association, deputy director of Tax Law Professional Committee of Guangdong Lawyers Association, and high-end tax talents in the first phase of China Certified Tax Agents Association (60 nationwide). Master of Accounting and Doctor of Law from Wuhan University, holds professional qualifications such as lawyer, accountant, certified tax accountant, Australian public accountant, certified asset appraiser, real estate appraiser, certified consulting engineer, financial economist, securities and fund practitioner.

Key practice areas :

corporate practices such as acquisition, merger and reorganization; Civil and commercial dispute resolution (litigation, arbitration and negotiation mediation); Tax law and taxation (compliance, planning, inspection response, reconsideration and litigation); Comprehensive legal and tax consultant (perennial and special); Investment and financing (VC, PE, large capital management); Cross-border commercial transactions and dispute resolution; real estate and construction projects.

Email:

wangyongjing@shengdian.com.cn

writing and examples: Cao wenwen

practice lawyer of shengdian law firm, member of shengdian tax law research center, Chinese tax agent. He has served in a large foreign financial leasing company and served as the legal department of the company's headquarters.

Key practice areas:

non-litigation matters such as mergers and acquisitions, tax law and taxation, capital markets and related dispute resolution.

Email:

caowenwen@shengdian.com.cn